United States Government Accountabilit

y

Office

GAO

Report to the Ranking Member,

Committee on Financial Services,

House of Representatives

TITLE INSURANCE

Actions Needed to

Improve Oversight of

the Title Industry and

Better Protect

Consumers

April 2007

GAO-07-401

What GAO Found

United States Government Accountability Office

Why GAO Did This Study

Highlights

Accountability Integrity Reliability

April 2007

TITLE INSURANCE

Actions Needed to Improve Oversight of

the Title Industry and Better Protect

Consumers

Highlights of

GAO-07-401, a report to the

Ranking Member, Committee on Financial

Services, House of Representatives

In a previous report and testimony,

GAO identified issues related to

title insurance markets, including

questions about the extent to

which premium rates reflect

underlying costs, oversight of title

agent practices, and the

implications of recent state and

federal investigations. This report

addresses those issues by

examining (1) the characteristics of

title insurance markets across

states, (2) factors influencing

competition and prices within

those markets, and (3) the current

regulatory environment and

planned regulatory changes. To

conduct this review, GAO analyzed

available industry data and studies,

and interviewed industry and

regulatory officials in a sample of

six states selected on the basis of

differences in size, industry

practices, regulatory environments,

and number of investigations.

What GAO Recommends

GAO recommends that HUD and

state insurance regulators take

actions to improve consumers’

ability to comparison shop for title

insurance and strengthen the

regulation and oversight of the title

insurance market, including the

collection of data on title agents’

operations. Further, Congress may

want to consider, as part of its

oversight of HUD, exploring the

need for modifications to RESPA,

including increasing HUD’s

enforcement authority. HUD

generally agreed with these

recommendations, and NAIC

agreed they should be explored.

The U.S. title insurance market is highly concentrated at the insurer level,

but market characteristics varied across states. In 2005, for example, five

insurers accounted for 92 percent of the national market, with most states

dominated by two or three large insurers. Variations across states included

the way title agents conducted their searches as well as the number of

affiliated business arrangements (ABA) in which real estate agents, brokers,

and others have a stake in a title agency. Finally, premiums varied across

states due to cost and market variations that can also make understanding

and overseeing title insurance markets a challenge on the national level.

Certain factors raise questions about the extent of competition and the

reasonableness of prices that consumers pay for title insurance. Consumers

find it difficult to comparison shop for title insurance because it is an

unfamiliar and small part of a larger transaction that most consumers do not

want to disrupt or delay for comparatively small potential savings. In

addition, because consumers generally do not pick their title agent or

insurer, title agents do not market to them but to the real estate and

mortgage professionals who generally make the decision. This can create

conflicts of interest if those making the referrals have a financial interest in

the agent. These and other factors put consumers in a potentially vulnerable

situation where, to a great extent, they have little or no influence over the

price of title insurance but have little choice but to purchase it.

Furthermore, recent investigations by the Department of Housing and Urban

Development (HUD) and state insurance regulators have identified instances

of alleged illegal activities within the title industry that appeared to take

advantage of consumers’ vulnerability by compensating realtors, builders,

and others for consumer referrals. Combined, these factors raise questions

about whether consumers are overpaying for title insurance.

Given consumers’ weak position in the title insurance market, regulatory

efforts to ensure reasonable prices and deter illegal marketing activities are

critical. However, state regulators have not collected the type of data,

primarily on title agents’ costs and operations, needed to analyze premium

prices and underlying costs. In addition, the efforts of HUD and state

insurance regulators to identify inappropriate marketing and sales activities

under the Real Estate Settlement Procedures Act (RESPA), have faced

obstacles, including constrained resources, HUD’s lack of statutory civil

money penalty authority, some state regulators’ minimal oversight of title

agents, and the increasing number of complicated ABAs. Finally, given the

variety of professionals involved in a real estate transaction, a lack of

coordination among different regulators within states, and between HUD

and the states, could potentially hinder enforcement efforts against

compensation for consumer referrals. Because of the involvement of both

federal and state regulators, including multiple regulators at the state level,

effective regulatory improvements will be a challenge and will require a

coordinated effort among all involved.

www.gao.gov/cgi-bin/getrpt?GAO-07-401.

To view the full product, including the scope

and methodology, click on the link above.

For more information, contact Orice M.

Williams at (202) 512-8678 or

Contents

Letter 1

Results in Brief 3

Background 7

Title Insurance Market Is Highly Concentrated at the Insurer Level,

but Otherwise Differs across States 11

Multiple Factors Raise Questions about the Extent of Competition

and the Reasonableness of Prices in the Title Insurance Industry 21

Limited State and Federal Oversight of the Title Insurance Industry

Has Resulted in Proposals for Change 41

Conclusions 53

Matters for Congressional Consideration 55

Recommendations for Executive Action 55

Agency Comments and Our Evaluation 56

Appendix I Objectives, Scope, and Methodology 59

Appendix II Potential Approach to Better Understand Title Agents’

Costs and How These Costs Relate to Insurance

Premiums

62

Appendix III Comments from the Department of Housing and Urban

Development 64

Appendix IV Comments from the National Association of Insurance

Commissioners 67

Appendix V GAO Contact and Staff Acknowledgments 68

Tables

Table 1: Information on Closed Cases and Settlements Involving

Referral Fees Resulting from Investigations by Insurance

Regulators in Six Sample States and HUD, 2003-2006 28

Page i GAO-07-401 Title Insurance

Table 2: Regulation of Title Insurance Agents in Six Sample States 44

Figures

Figure 1: Title Insurer National Market Share as a Percentage of

Direct Premiums Written, 2005 12

Figure 2: Title Insurance Premiums Written, by Source, 2005 14

Figure 3: Example of an Affiliated Business Arrangement 15

Figure 4: Common Elements of the Title Search and Examination

Process 16

Figure 5: Title Insurance Premium Rates for a Basic Owner’s Policy

on Median-Priced Homes in Selected Areas, 2005 19

Figure 6: Average Allocation of Closing Costs in California, 2005 24

Figure 7: Example of an Alleged Captive Reinsurance Arrangement 31

Figure 8: Combined Return on Equity for the Five Largest Title

Insurers, and the Property-Casualty Insurance Industry as

a Whole, 1992-2005 36

Figure 9: Percentage Change in Premium Rates and Premiums Paid

on Median-Priced Homes in Selected Areas in Five Sample

States, 2000-2005 37

Figure 10: Typical Premium Splits between Insurers and Agents in

Six Sample States 39

Figure 11: Title Industry Costs as a Percentage of Premiums

Written, 2005 42

Page ii GAO-07-401 Title Insurance

Abbreviations

ABA affiliated business arrangement

ALTA American Land Title Association

Fannie Mae Federal National Mortgage Association

Freddie Mac Federal Home Loan and Mortgage Corporation

HUD Department of Housing and Urban Development

NAIC National Association of Insurance Commissioners

RESPA Real Estate Settlement Procedures Act

RESPRO Real Estate Services Providers Council

SEC Securities and Exchange Commission

This is a work of the U.S. government and is not subject to copyright protection in the

United States. It may be reproduced and distributed in its entirety without further

permission from GAO. However, because this work may contain copyrighted images or

other material, permission from the copyright holder may be necessary if you wish to

reproduce this material separately.

Page iii GAO-07-401 Title Insurance

United States Government Accountability Office

Washington, DC 20548

April 13, 2007

The Honorable Spencer Bachus

Ranking Member

Committee on Financial Services

House of Representatives

Dear Mr. Bachus:

Title insurance is designed to guarantee clear ownership of a property that

is being sold and is a required part of most real estate transactions across

the United States. Although home buyers pay for title insurance premiums,

they often know little about the insurers themselves or the title insurance

industry. Recent state and federal investigations into the sale of title

insurance have identified practices by some title insurers, their agents, and

others involved in the sale of title insurance, that allegedly allowed these

entities to make undue profits at consumers’ expense. At the same time,

insurance regulators in at least four states have concluded that consumers

are being overcharged for title insurance, and the California insurance

regulator has recommended rate rollbacks—an action that some in the

title industry have strongly criticized. Because virtually everyone who

buys a home or refinances a home mortgage in the United States typically

must purchase title insurance, the potential effects of such practices are

enormous.

We previously provided a report and testimony identifying issues in the

title insurance market that merited further study because they could shed

light on competition and the prices consumers pay.

1

In response to the

former Chairman’s request, we prepared this report to address and

elaborate on those issues. Specifically, we address (1) the characteristics

of title insurance markets and differences across states, (2) prices and

competition in the industry, and (3) the current regulatory environment

and planned regulatory changes.

1

GAO, Title Insurance: Preliminary Views and Issues for Further Study, GAO-06-568

(Washington, D.C.: Apr. 24, 2006); and Title Insurance: Preliminary Views and Issues for

Further Study

, GAO-06-569T (Washington, D.C.: Apr. 26, 2006).

Page 1 GAO-07-401 Title Insurance

To do this work, we performed a detailed review of the laws, regulations,

and market practices in California, Colorado, Illinois, Iowa, New York, and

Texas.

2

We chose these six states on the basis of differences in the size of

their markets, title insurance practices and customs, the rate-setting and

regulatory environments, and the number of federal and state investigative

actions. In some of these states, we were able to tour title plant facilities

and observe the title search and examination process. We reviewed

available studies of the title insurance industry and discussed their results

with the authors.

3

We also gathered the views of officials from a variety of

national organizations whose members are involved in the marketing or

sale of title insurance or related activities, and we spoke with insurers,

agents, and title industry associations. We asked for, but did not receive,

cost data from agents and insurers that would allow us to analyze agents’

costs. We obtained and analyzed data collected by the National

Association of Insurance Commissioners (NAIC), the Texas Department of

Insurance, the California Department of Insurance, and the American Land

Title Association (ALTA).

4

We also consulted other publicly available

financial information on title insurers and agents and spoke with agents

about costs, examined financial data filed with the Securities and

Exchange Commission (SEC), and spoke with officials from three of the

largest title insurance underwriters. We interviewed key insurance,

banking, mortgage, and real estate regulators in each state about the

regulatory environments, spoke to officials from the Department of

Housing and Urban Development (HUD), and reviewed relevant federal

laws and regulations. We also discussed these issues with officials from

the Federal National Mortgage Association and the Federal Home Loan

and Mortgage Corporation to better understand the relationship between

the secondary mortgage market and title insurance. Lastly, we interviewed

2

Except where noted, our analysis is limited to these states.

3

Birny Birnbaum, Report to the California Insurance Commissioner: An Analysis of

Competition in the California Title Insurance and Escrow Industry (Austin, TX:

December 2005); Donald Martin, PhD, and Richard Ludwick, Jr., PhD, Affiliated Business

Arrangements and Their Effects on Residential Real Estate Settlement Costs: An

Economic Analysis (Washington, D.C.: October 2006); and Gregory Vistnes, An Economic

Analysis of Competition in the Title Insurance Industry (Washington, D.C.: March 2006).

4

NAIC is a voluntary organization of the chief insurance regulatory officials of the 50 states,

the District of Columbia, and the four U.S. territories. NAIC assists state insurance

regulators by providing guidance, model (or recommended) laws and guidelines, and

information-sharing tools. ALTA is a national trade association for title insurers and agents,

but its members may also include attorneys, builders, developers, lenders, and real estate

brokers.

Page 2 GAO-07-401 Title Insurance

staff and state regulators working with NAIC to get their views on the

industry and to obtain information on the activities of their Title Insurance

Working Group.

We performed our work in Washington, D.C.; Chicago, Illinois; and six

sample states between February 2006 and March 2007 in accordance with

generally accepted government auditing standards. Appendix I contains a

more detailed description of our objectives, scope, and methodology.

In the United States, the title insurance market is highly concentrated at

the insurer (or underwriter) level, but market characteristics varied across

the states. In 2005, for example, five insurers accounted for 92 percent of

the national market, and most states were dominated by two or three large

insurers. However, state markets differed in several ways. For example,

large insurers tended to use local or regional title agents to conduct their

business, and the mix of affiliated agents (those in which the insurer has

an ownership interest) and independent agents varied across states. The

extent of affiliated business arrangements (ABA)—situations in which real

estate or other professionals are part or full owners of title agencies—also

varied. In some states the number of ABAs, which have been cited in many

of the regulatory investigations into industry practices, has grown

substantially. Furthermore, title agents use different processes to carry out

title searches and examinations, largely because of variations in the way

the industry has developed across states. Title agents in some states have

automated “title plants” containing most public records, while, in other

states, title agents rely on the less-efficient process of hiring people to

search physical records. The extent of agents’ activities also varied widely

across states, including how they set prices for their services, the portion

of claims they paid, and the extent of their participation in the escrow and

closing processes. Finally, we found that premiums varied across states,

due to cost and market variations that can make understanding and

overseeing title insurance markets a challenge on the national level.

Results in Brief

Several factors related to the way that title insurance is marketed and

priced raise questions about the extent of price competition in the title

insurance industry and the ability of consumers to affect market prices.

First, consumers find it difficult to shop for title insurance based on price.

Purchasing title insurance is a transaction that consumers are unfamiliar

with, and it can be difficult for them to gather information on all title

insurance-related costs. HUD provides educational information on title

insurance. However, the benefit of this information is limited because

consumers may receive it after a title agent and insurer have been

Page 3 GAO-07-401 Title Insurance

selected, and lenders are not required to provide it on mortgage refinance

transactions. In addition, purchasing title insurance is generally a small

part of a larger home purchase or mortgage refinancing process that most

consumers do not want to disrupt or delay for relatively small potential

savings. Second, consumers generally do not select their title agent or

insurer, and title agents do not market to consumers but rather compete

among themselves for referrals from those who do—that is, real estate and

mortgage professionals. This arrangement can create conflicts of interest

if professionals making the referrals have a financial interest in the agent

recommended. HUD and state insurance regulators have recently

identified instances of alleged illegal activities within the title industry that

appeared to compensate real estate agents, builders, and others for

referring consumers to particular title insurers or agents. These alleged

activities, which include referral fees, captive reinsurance arrangements,

and inappropriate ABAs, potentially reduce price competition and,

according to some insurance regulators, could indicate excessive pricing

by insurers.

5

Third, as property values or loan amounts increase, prices

that consumers paid for title insurance appeared to increase faster than

insurers’ and agents’ costs. Insurers we spoke with argued that such a

pricing structure reflected regulators’ intent to subsidize consumers in

low-value transactions, but they could not provide data to support the

existence of such subsidization. Of the six regulators we spoke with, only

one said that such subsidization was intentional. Finally, in states where

agents’ search and examination services are not included in the premium,

it is not clear that the underlying costs justify the additional amounts

consumers may pay to title agents. Insurers told us that they generally

shared the same portion of premiums with their agents, regardless of

whether agents’ costs for search and examination services were to be

included in the premium. Ultimately, disagreement exists between title

industry officials and regulators over the actual extent of price

competition within title insurance markets. Industry officials generally

assert that price competition exists, while many regulators argue (1) that it

does not exist and (2) that consumers may be paying too much for title

insurance compared with the cost of providing the insurance.

5

In captive reinsurance arrangements, a home builder, real estate broker, lender, title

insurance company, or some combination of these entities forms a reinsurance company

that works in conjunction with a title insurer. Sham ABA arrangements are those in which

the affiliated entity performs little or no actual settlement services and is allegedly being

used just to compensate ABA owners for consumer referrals. Other arrangements include

the use of inducements and incentives by title companies to obtain title insurance business,

especially when these inducements were used to influence referrals by real estate agents,

banks, lenders, builders, developers, and others.

Page 4 GAO-07-401 Title Insurance

Data collection efforts and regulatory oversight, especially of title agents,

were limited across the states we reviewed. Given consumers’ apparently

limited ability to exert pressure on title agents and insurers to compete on

price, the critical question is whether amounts paid by consumers for title

insurance reflect the actual underlying costs of producing title insurance

policies. Potentially understanding the relationship between costs and the

amounts consumers pay could help regulators improve their ability to

protect consumers. Yet, states rarely audit agents; few require strong

insurer oversight of agents; and, until recently, state regulators had done

little to oversee ABAs or enforce laws intended to restrict business from

affiliated sources. Also, because title insurance is a relatively small line of

insurance, title insurers and agents get less than the usual limited market

conduct scrutiny given other types of insurers by state insurance

regulators.

6

All of the regulators, both state and federal, face a number of

challenges. For example, varying levels of cooperation exist within each

state among the regulators who oversee entities involved in the sale and

marketing of title insurance, with some states demonstrating little or no

cooperation and others having somewhat more structured arrangements.

HUD—the primary federal agency responsible for enforcing the Real

Estate Settlement Procedures Act (RESPA)—has taken a number of

enforcement actions under RESPA recently, but HUD officials told us that

they face resource limitations and difficulties in investigating increasingly

complex ABA arrangements. Furthermore, HUD is authorized to seek

injunctions against alleged violations of section 8 of RESPA’s provisions

on referral fees and affiliated businesses, but HUD is not authorized to

levy civil money penalties. Moreover, a lack of formal coordination

between HUD and state regulators on referral fee cases may have hindered

enforcement efforts. In response to these and other concerns, several state

regulators and HUD are either planning or making changes to their

regulatory regimes for the marketing and sale of title insurance. These

changes include potentially reducing premium rates; collecting detailed

cost data from title agents; and seeking changes to RESPA, including

enhancing HUD’s enforcement authority. Some industry stakeholders see

the current model of selling and marketing title insurance as irretrievably

broken and have put forth the following two alternatives: (1) requiring

6

Market conduct examinations are performed by state insurance commissioners, and they

review agent-licensing issues, complaints, types of products sold by the company and

agents, agent sales practices, proper rating, claims handling, and other market-related

aspects of an insurer’s operation. See GAO, Insurance Regulation: Common Standards

and Improved Coordination Needed to Strengthen Market Regulation,

GAO-03-433

(Washington, D.C.: Sept. 30, 2003).

Page 5 GAO-07-401 Title Insurance

lenders to pay for title insurance and (2) following the Iowa model of a

state-run title insurer.

We are recommending that HUD take two actions to improve the

functioning of the title insurance market. Specifically, we are

recommending that HUD (1) improve consumers’ ability to shop for title

insurance based on price and (2) improve its ability to detect and deter

violations of section 8 of RESPA. In taking these actions, we recommend

that HUD consider expanding the information in its home-buyer

information booklet; evaluating the costs and benefits to consumers from

ABAs; clarifying regulations related to referral fees and ABAs; and

enhancing the agency’s coordination with state regulators. Likewise, we

are recommending that state insurance regulators, working through NAIC

where appropriate, take two actions to improve the functioning of the title

insurance market. Specifically, we are recommending that state regulators

take action to (1) improve consumers’ ability to shop for title insurance

and (2) improve their oversight of title agents. As part of this process, we

are recommending that these regulators consider evaluating the

competitive benefits of publicizing complete title insurance cost

information; strengthening their regulation of title agents and ABAs,

including the collection of data on title agents’ operations; and exploring

ways to improve their cooperation with other state regulators and HUD.

We also suggest, as a matter for congressional consideration, amending

RESPA to give HUD increased enforcement authority for violations of

RESPA’s section 8 prohibitions on referral fees by granting the ability to

levy civil money penalties and enhance the information required to be

provided to consumers.

We provided a draft copy of this report to HUD and NAIC. The Assistant

Secretary for Housing at HUD and the Executive Vice President of NAIC

provided written comments on the draft. Their comments are included in

appendixes III and IV, respectively, of this report. The Assistant Secretary

for HUD generally agreed with the recommendations in the report, and

also indicated that the report accurately assessed the issues that adversely

affect consumers in the title insurance market. In response to our

recommendation to better protect consumers and improve their ability to

shop for title insurance, he acknowledged the importance of these goals

and noted that HUD is taking several actions in these areas. Specifically,

he said that HUD is (1) considering ways to improve its home-buyer

information booklet; (2) evaluating whether various ABA structures, even

though they may be legal, are operating as Congress intended; and

(3) continuing its efforts to develop and clarify guidelines regarding

practices that negatively effect consumers. With respect to our

Page 6 GAO-07-401 Title Insurance

recommendation to consider improving regulatory coordination with state

regulator agencies, the Assistant Secretary agreed that such coordination

is necessary and pointed out past instances of successful cooperation

between HUD and state insurance regulators. Lastly, he emphasized the

ongoing challenge of RESPA enforcement without civil money penalty

authority, stating that consumers would benefit if such authority were

granted to HUD. The Executive Vice President of NAIC stated that the

recommendations in the report were worthy of exploration, and she noted

that the report recognizes that shortcomings exist in the area of consumer

protection. Both HUD and NAIC also offered clarifying remarks.

In any real estate transaction, the lender providing the mortgage needs a

guarantee that the buyer will have clear ownership of the property. Title

insurance is designed to provide that guarantee by generally agreeing to

compensate the lender (through a lender’s policy) or the buyer (through

an owner’s policy) up to the amount of the loan or the purchase price,

respectively. Lenders also need title insurance if they want to sell

mortgages on the secondary market, since they are required to provide a

guarantee of ownership on the home used to secure the mortgage.

7

As a

result, lenders require borrowers to obtain title insurance for the lender as

a condition of granting the loan (although the buyer, the seller, or some

combination of both may actually pay for the lender’s policy). Lenders’

policies are in force for as long as the loan is outstanding, but end when

the loan is paid off (e.g., through a refinancing transaction); however,

owners’ policies remain in effect as long as the purchaser of the policy

owns the property.

Background

Title insurance is sold primarily through title agents, although insurers

may also sell policies themselves. Before issuing a policy, a title agent

checks the history of a title by examining public records, such as deeds,

mortgages, wills, divorce decrees, court judgments, and tax records. If the

title search reveals a problem, such as a tax lien that has not been paid, the

agent arranges to resolve the problem, decides to provide coverage despite

the problem, or excludes it from coverage. The title policy insures the

policyholder against any claims that might have existed at the time of the

purchase but were not identified in the public record. The title policy does

7

Both the Federal National Mortgage Association and the Federal Home Loan Mortgage

Corporation require a guarantee of title as a condition of purchasing loans from mortgage

lenders.

Page 7 GAO-07-401 Title Insurance

not require that title problems be fixed, but compensates policyholders if a

covered problem arises. Except in very limited instances, title insurance

does not generally insure against title defects that arise after the date of

sale.

Title searches are generally carried out locally because the public records

to be searched are usually only available locally. Title agents or their

employees conduct the searches. The variety of sources that agents must

check during a title search has fostered the development of privately

owned, indexed databases called “title plants.” These plants contain copies

of the documents obtained through searches of public records, and they

index the copies by property address and update them regularly. Insurers,

title agents, or a combination of entities may own a title plant. In some

cases, owners allow other insurers and agents access to their plants for a

fee.

Title insurance premiums are paid only once, at the time of sale or

refinancing, to the title agent. In what is called a premium split, agents

retain or are paid a portion of the premium amount as a fee for conducting

the title search and related work and for their commission. Agents have a

fiduciary duty to account for premiums paid to them, and insurers

generally have the right to audit the agents’ relevant financial records. The

party responsible for paying for the title policies varies by state and even

by areas within states. In many cases, the seller pays for the owner’s policy

and the buyer pays for the lender’s policy, but the buyer may also pay for

both policies or split some or all of the costs with the seller. In most cases,

the owner’s and lender’s policies are issued simultaneously by the same

insurer, so that the same title search can be used for both policies. The

price that the consumer pays for title insurance is determined by applying

a rate set by the underwriter or state to the loan value (for the lender’s

policy) and home price (for the owner’s policy). In a recent nationwide

survey, the average cost for simultaneously issuing lender’s and owner’s

policies on a $200,000 loan, plus other associated title costs, was

approximately $859, or approximately 28 percent of the average total loan

origination and closing fees.

8

8

Bankrate.com, Closing Costs Survey,

http://www.bankrate.com/brm/news/mortgages/ccmain2006a1.asp (North Palm Beach, FL:

August 2006). The survey was conducted by Bankrate.com in 2006 by obtaining online

information where available. We did not assess the validity of the data collected in the

survey.

Page 8 GAO-07-401 Title Insurance

Title insurance differs from other types of insurance in key ways. First, in

most property and casualty lines, losses incurred by the underwriter

account for most of the premium. For example, property-casualty insurers’

losses and loss adjustment expenses accounted for approximately 73

percent of written premiums in 2005.

9

In contrast, losses and loss

adjustment expenses incurred by title insurers as a whole were

approximately 5 percent of the total premiums written, while the amount

paid to or retained by agents (primarily for work related to title searches

and examinations and for commissions) was approximately 70 percent.

Second, title agents’ roles and responsibilities differ from those of agents

for other lines of insurance. Agents in lines of insurance other than title

insurance primarily serve as salespeople, while title agents’ work can be a

labor-intensive process of searching, examining, and clearing property

titles as well as underwriting and traditional sales and marketing. Title

agents access and examine numerous public documents, among them tax

records, liens, judgments, property records, deeds, encumbrances, and

government documents, and then clear or exclude from coverage any title

problems that emerge. Depending on the level of technology used, the

accessibility of public documents, the relative efficiency of local

government recorders’ offices, and other factors, this process can take

from a few minutes up to a few weeks or more. In some states, title agents

also are responsible for claims up to a specific dollar amount. Most title

agents also handle the escrow and closing processes and document

recordation after the closing. In general, title agents issue the actual

insurance policy and, after deducting expenses, remit the title insurer’s

portion of the premium.

Third, unlike premiums for other types of insurance, title insurance

premiums are nonrecurring. That is, title insurers have only one chance to

capture the cost of the product from the consumer, unlike other types of

insurers that collect premiums at regular intervals for providing ongoing

coverage. The title insurance premium amount must cover losses for any

future problems that were either not uncovered in the title agent’s search

or, for a small number of policies, problems that emerge after the day of

closing.

9

According to industry experts and analysts, the different loss and expense structure of the

title insurance industry reflects the fact that title insurance is primarily focused on

preventing losses through title searches and examinations, and that most property-casualty

insurance is focused on compensating policyholders for losses.

Page 9 GAO-07-401 Title Insurance

Fourth, title insurance has a different coverage period than other types of

insurance. With title insurance, coverage begins on the day of closing and

goes back in time. Most policies cover events that occurred in the past,

including unpaid tax liens, judgments, issues with missing heirs, and

forgeries in the document chain of title. The purpose of the title agent’s

search is to turn up these problems before closing so that they can be

cleared or excluded from coverage. However, if a problem occurred in the

past but only emerged after the day of closing and was not excluded from

coverage, then the policy would offer protection to the lender and home

owner. The comprehensiveness of the agent’s search can be a factor in

minimizing such losses. For this reason, title insurance is often referred to

as loss prevention insurance, in contrast to other types of insurance that

attempt to prospectively minimize exposure to claims.

Finally, the title insurance market’s business cycle is more closely related

to the real estate market and to interest rates than the business cycle for

other types of insurance. Typically, this relationship is inverse, so that the

revenues of title companies rise when interest rates fall, largely because

lower interest rates usually lead to a surge in home buying and refinancing

and thus increase demand for title services and products.

Under current federal law, the regulation of insurance, including title

insurance, is primarily the responsibility of the states. However, title

insurance entities are also subject to RESPA, a federal law intended to

improve the settlement process for residential real estate. Section 8 of

RESPA generally prohibits the giving or accepting of kickbacks and

referral fees among persons involved in the real estate settlement process.

Section 8 also lays out the conditions under which ABAs are permissible.

First, the affiliation must be disclosed to the consumer, along with a

written estimate of charges. Second, ABA representatives may not require

consumers to use a particular settlement service provider. Third, the only

thing of value that ABA owners may receive, other than payment for

services rendered, is a return on their ownership interest. In addition,

HUD has issued policy statements that describe multiple factors, including

what it considers to be core title services, that HUD will use in

determining if an entity is a bona fide provider of settlement services. HUD

is responsible for administering section 8 of RESPA, but its enforcement

authority is limited to seeking injunctions against potential violations.

Unlike other sections of RESPA (e.g., section 10, which authorizes HUD to

assess civil money penalties for certain violations by entities that fail to

provide escrow account statements), section 8 of RESPA does not

authorize HUD to levy civil money penalties for violations.

Page 10 GAO-07-401 Title Insurance

Title Insurance

Title insurance markets can be described by various characteristics, such

as the following:

• While high market concentration exists among national title insurers, they

market insurance through large numbers of independent and affiliated

agents, with the mix varying across states.

• The use of ABAs—in which a real estate professional, such as a real estate

agent, owned a share of a title agency—varied.

Title Insurance

Market Is Highly

Concentrated at the

Insurer Level, but

Otherwise Differs

across States

• Processes used by agents to conduct searches and examinations in some

states were more efficient than others, and the responsibilities of title

agents also varied.

• Premiums across states are difficult to compare, but they appeared to vary

significantly.

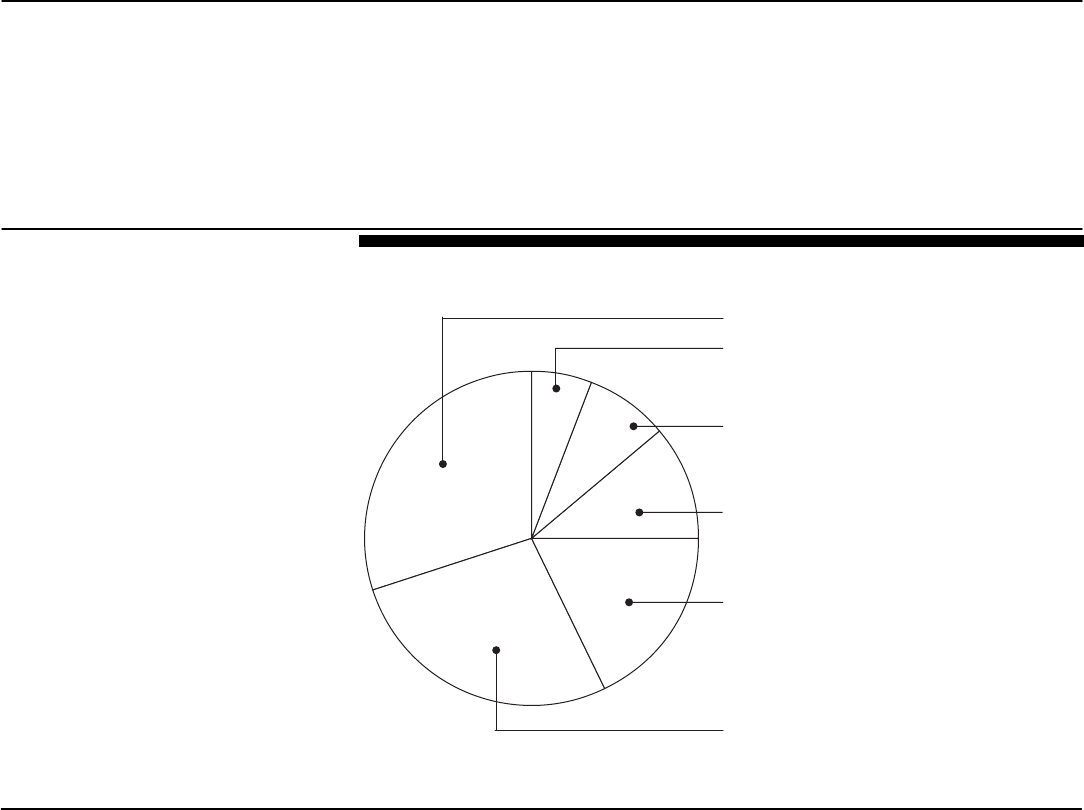

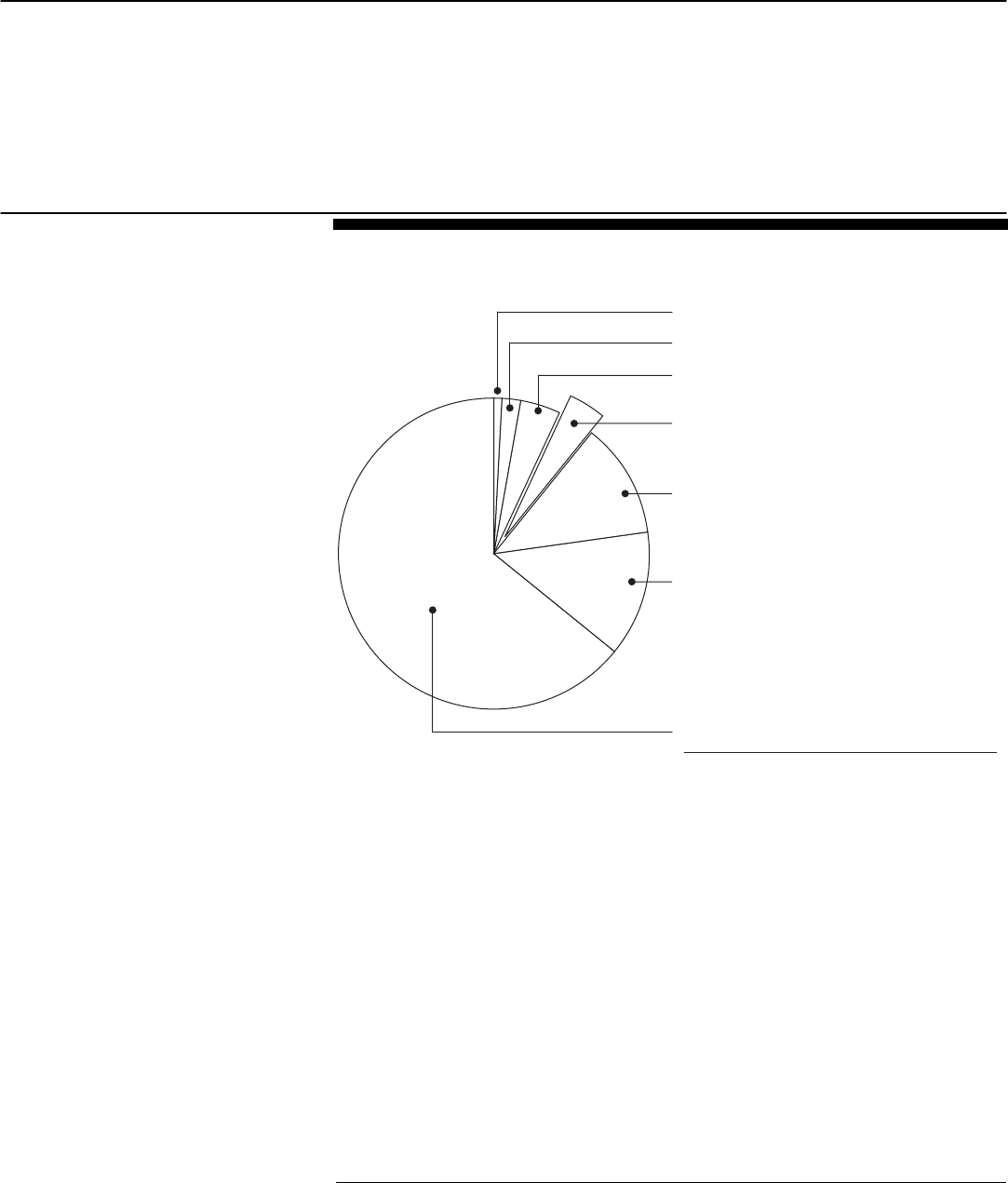

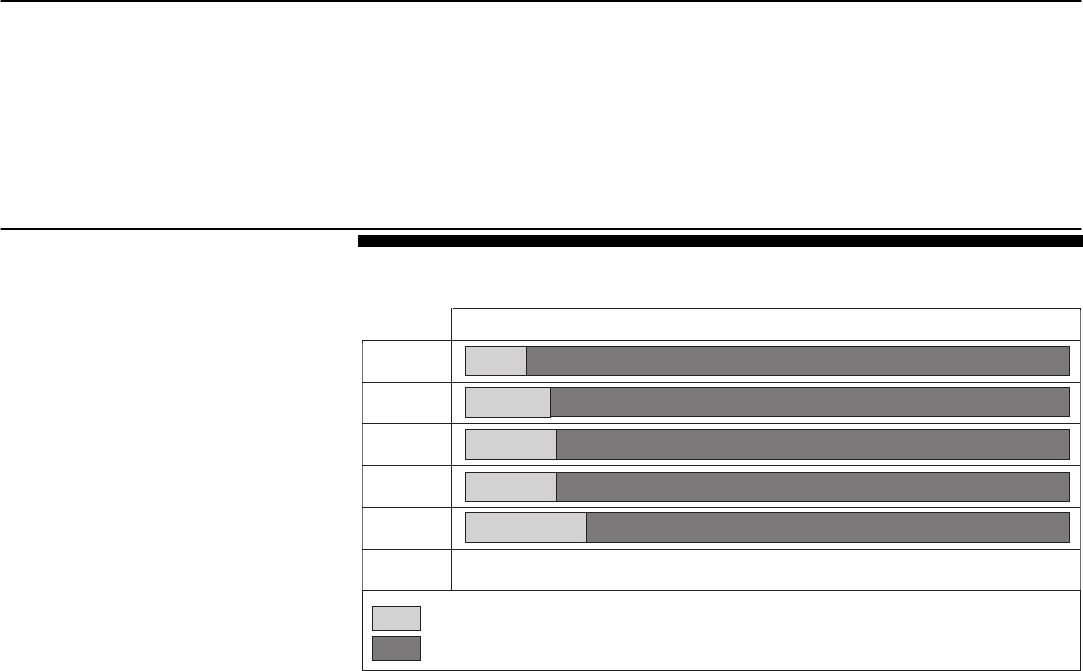

Nationally, five title insurers, or underwriters, captured about 92 percent

of the market in 2005 (see fig. 1). Most states were dominated by a group

of two or three insurers, sometimes including a regional insurer. For

example, in California, about 66 percent of the market share in 2005 was

split nearly evenly between the largest two insurers—First American and

Fidelity. The remaining approximately 33 percent of the market was

predominantly split among the other three national insurers (25 percent)

and five regional independent insurers (8 percent). Although they are

national insurers, these five major underwriters sell and market title

insurance in local markets through networks of direct operations, partial

or full ownership of affiliates, and contracts with independent agents.

According to the annual reports of the four largest title insurers, they each

use between 8,000 and 11,000 agencies to sell their insurance nationwide.

Page 11 GAO-07-401

Figure 1: Title Insurer National Market Share as a Percentage of Direct Premiums

Written, 2005

Note: Total may not add up to 100 percent due to rounding.

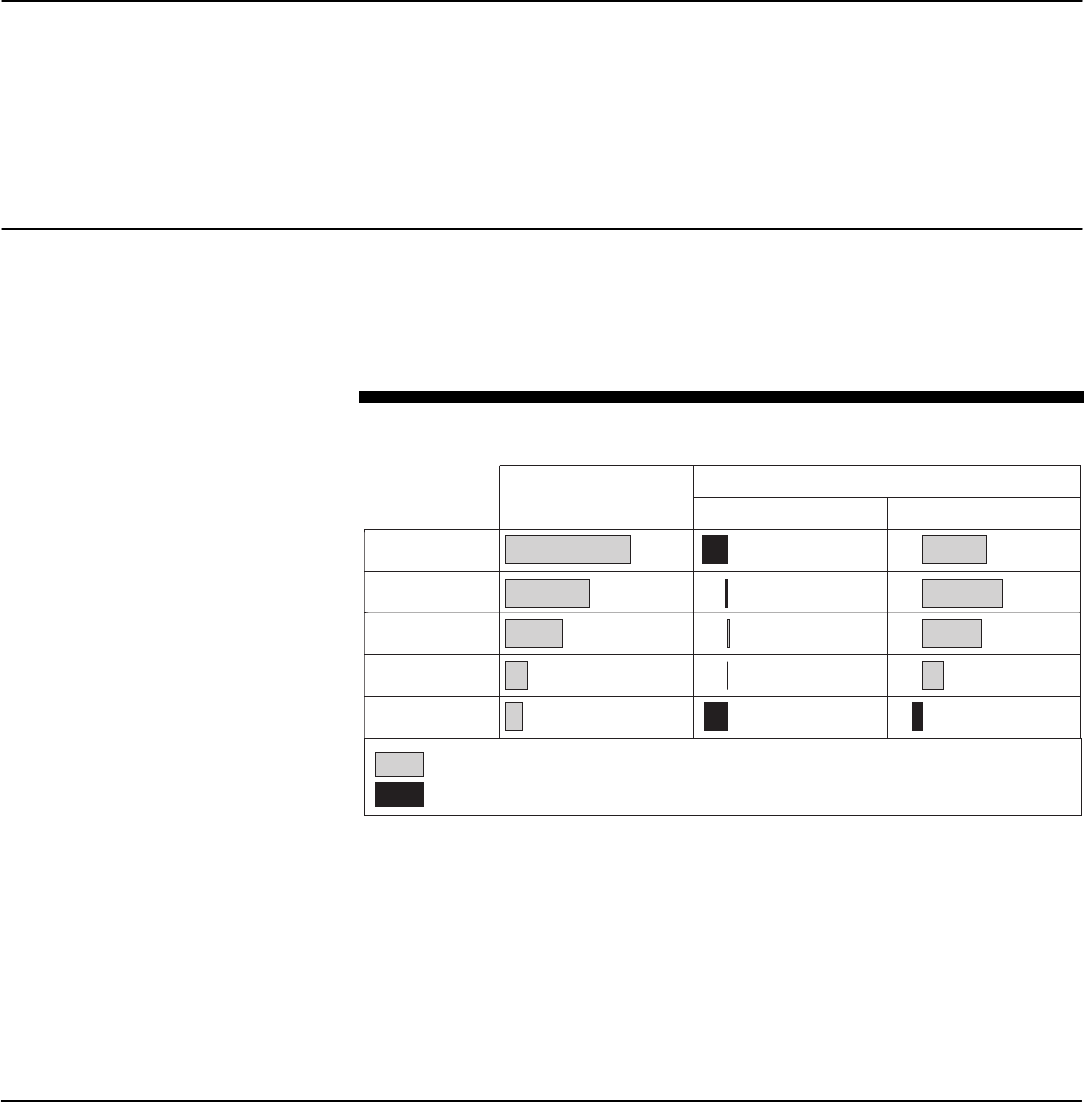

Most state markets have two types of title agents: affiliated and

independent. Title insurers use both types of agents, depending on

conditions in the local market, including local tax policies and established

market practices, as well as the level of service the underwriter provides

to the agents. Affiliated agents carry higher fixed costs to the insurer as

owner, and underwriters told us that these costs were especially

challenging when the market softened and the insurer’s tax liability for

affiliated agents rose. However, insurers also said that with affiliated

agents they had more control over the premium split and, because the

agents were closely aligned with the underwriter, did not have to provide

as much in services, such as training. Underwriters noted that they also

benefited from contracting with independent agents because doing so kept

their fixed costs low and allowed them to benefit from some tax

advantages. However, according to the insurers, contracting has its

disadvantages, by obliging the insurers to negotiate a competitive premium

split (in nonpromulgated states) or risk having the agent establish a

6%

8%

Old Republic

11%

18%

27%

29%

Source: GAO analysis of industry data.

All other insurers

Stewart

Land America

First American

Fidelity

Mix of Affiliated and

Independent Agents

Differs by State

Page 12 GAO-07-401 Title Insurance

relationship with another underwriter.

10

Independent agents, who work

with several underwriters, also may not provide the guaranteed flow of

business, and thus the same revenue stream, as affiliated agents.

Underwriters balance these benefits and risks when determining which

agents they will use in each state. Two underwriters told us that they strive

to maintain about an equal balance between affiliated agents and

independent agents. Other insurers told us that, because their expenses

can be higher by virtue of their ownership interest in affiliated agents, they

were reluctant to take on too many affiliated agents and preferred to

contract with independent agents, especially when market conditions

declined. However, several industry participants told us that underwriters’

purchase and use of affiliated agents in some states had increased

significantly over the last 5 years. As shown in figure 2, affiliated agents

dominated the market in California, the state with the largest total of

premiums written, while independent agents capture the majority of the

markets in Colorado, Illinois, and New York. Conversely, the Texas market

was relatively more evenly balanced, with insurers, affiliated agents, and

independent agents sharing the number of premiums written. In Iowa, the

state-run Title Guarantee Division of the Iowa Finance Authority has a

slight majority of the market and independent agents have most of the

remainder.

10

The term “nonpromulgated states” refers to those states where the title rate is determined

by a method other than a state regulatory body setting it.

Page 13 GAO-07-401 Title Insurance

Figure 2: Title Insurance Premiums Written, by Source, 2005

Iowa

Total

Colorado

Illinois

New York

Texas

California

4.5

$980.9

35.5

71.5

301.9

459.2

$108.4

$6,608.7

8.5

343.2

350.7

1,220.6

1,487.5

$3,198.3

44

9

22

13

2

28

74

Premiums

Written directly

by insurer

$2,928.4

0.8

75.4

45.4

25.6

410.6

$2,370.7

Written by

affiliated

agents

3.2

232.3

233.8

893.1

617.7

$719.1

$2,699.3

Written by

independent

agents

Total

Percentage of premiums for the state, by writer

Source: GAO analysis of title industry data.

15

53

10

20

25

31

3

41

38

68

67

73

42

23

a

Dollars in millions

a

Premiums listed as being written directly by insurer are those written by the state-run Title Guarantee

Division of the Iowa Finance Authority. Premiums written by affiliated or independent agents are

premiums written by out-of-state title insurers on properties in Iowa.

Use of Affiliated Business

Arrangements Appears to

Be Increasing

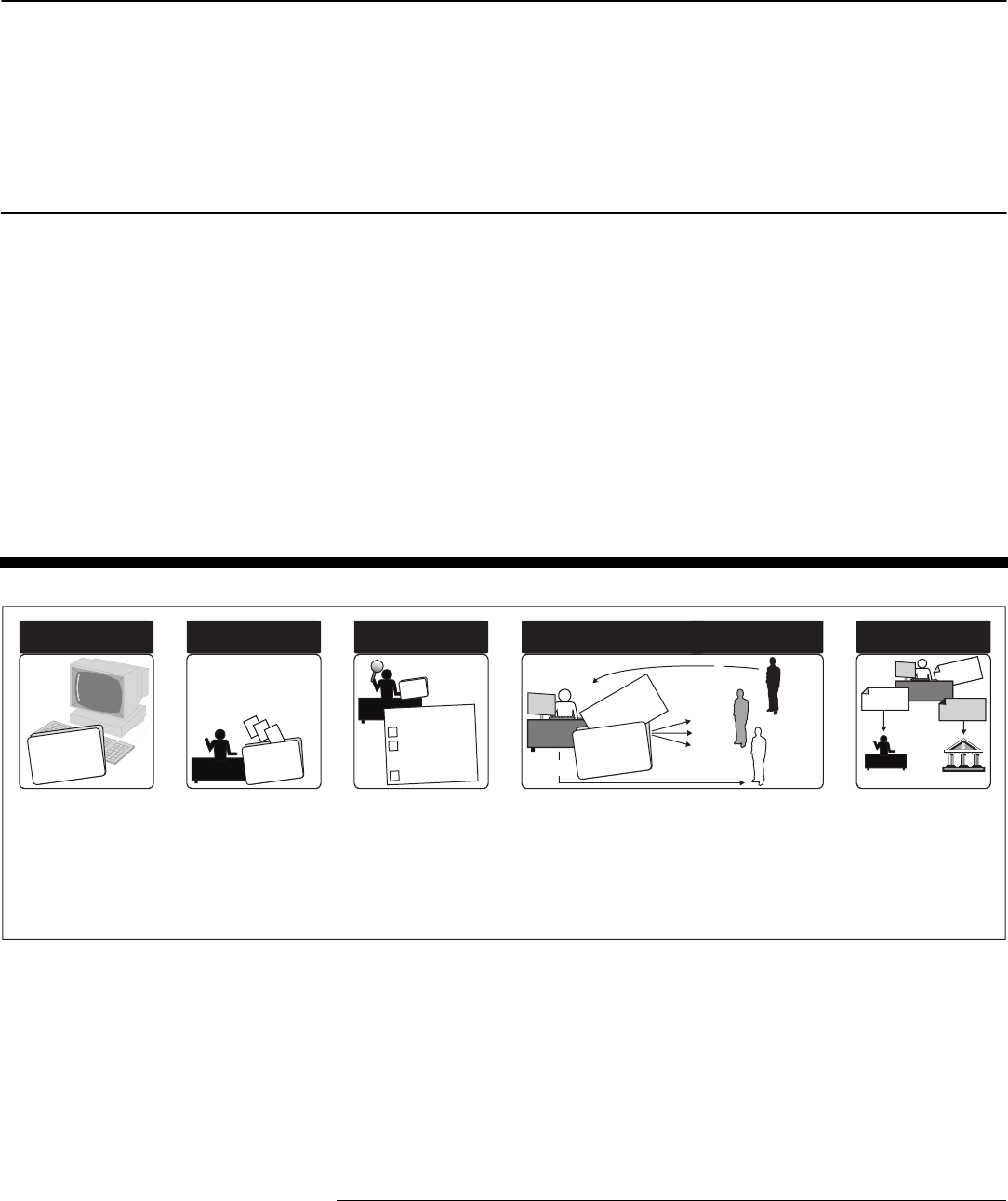

We found that the use of ABAs varied by insurer and location. ABAs

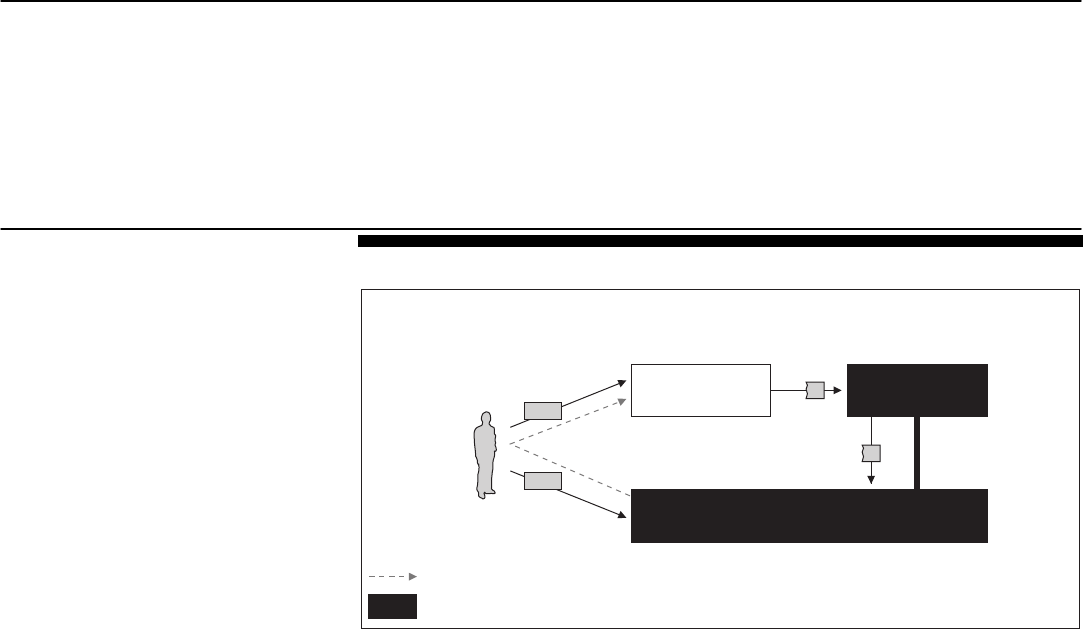

generally involved a referring entity, such as a real estate or mortgage

professional, or builder, having full or partial ownership of an agency (see

fig. 3). For example, a mortgage lender and a title agent might form a new

jointly owned title agency, or a builder might buy a portion of a title

agency. The owners of ABAs are to split the revenues in proportion to

their ownership shares to satisfy antirebating laws.

Page 14 GAO-07-401 Title Insurance

Figure 3: Example of an Affiliated Business Arrangement

A

B

$

Referring entity refers

customers to title agency

that is part of affiliated

business arrangement

Ownership interest

Title agency profits

and sends portion

to referring entity

Referring entity

$

A

B

Entity that refers customers

Title agency receiving referred business

Ownership interest

Path of referred customers

Profit made from referred customers

Customers

$

Source: GAO analysis of interviews with industry officials.

General structure and flow

Title agency

Partially owned by

the referring entity

Nationally, the use of ABAs appears to be growing. For example,

according to a study done for the Real Estate Services Providers Council

(RESPRO), affiliated title agents accounted for approximately 26 percent

of title-related closing costs in 2005, up from about 22 percent in 2003.

11

Although precise data showing state-by-state growth were not available,

industry participants in some states—especially Colorado, Illinois,

Minnesota, and Texas—told us that the number of ABAs in their states had

grown significantly.

12

11

RESPRO is a national nonprofit trade association of settlement service providers,

including real estate broker-owners, real estate franchisers, mortgage lenders/brokers, title

insurers/agents, home builders, and home warranty companies. Many of its members offer

affiliated services through subsidiaries, joint ventures, and partnerships.

12

Although Minnesota was not in our sample, we spoke to state insurance regulators in the

state.

Page 15 GAO-07-401 Title Insurance

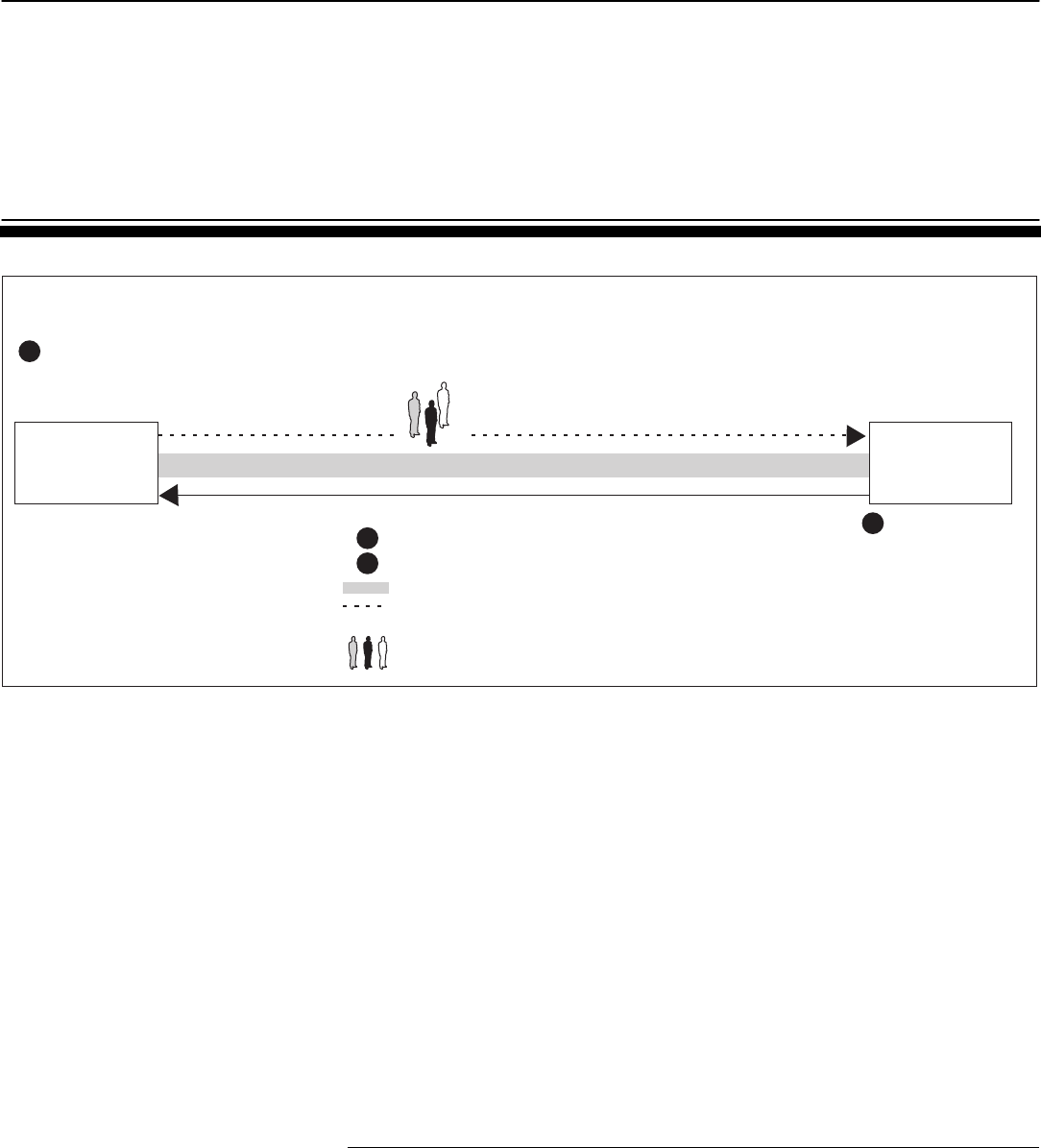

We found that while the basic title search and examination process shared

certain elements across states, the process was more efficient in some

states than in others. Figure 4 describes the common elements of the title

search and examination process, which begins with a request from the

consumer’s representative and intake by the title agent. The agent then

performs the search, and a title examiner hired by the title agent analyzes

the collected documents to identify any potential problems to be cleared.

Once any identified problems are cleared, exempted from coverage, or

insured over, the title agent prepares the closing documents and collects

and disburses checks at the closing. Finally, the agent deposits collected

funds in escrow accounts, records the deed or title with the relevant local

government offices, and submits the title commitment to the insurer for

policy issuance.

Agents Conduct the Title

Search and Examination

Process Differently across

States

Figure 4: Common Elements of the Title Search and Examination Process

Deed

Title order received from

consumer representative

(real estate agent,

mortgage broker, attorney,

other representative).

Information about all

interested parties entered

into data system

and verified.

Property identified in

local government

records and search

performed for all

pertinent property

title documents.

Title agent deposits

collected funds,

takes deed for recording,

produces policy, and

submits risk portion of title

insurance premium

to underwriter.

Title examiner analyzes

all documents and identifies

problems. Problems are

cleared, exempted from

coverage, or insured over.

Title agent prepares title commitment and other

necessary closing documents and distributes them

to involved parties. Title agent, closer, or escrow

officer collects/disburses funds

with involved parties.

Intake/Request

Identification/

Search

Analysis and repair Completion

Closing

Sources: GAO observation of title plant operations and analysis of comments made by title industry officials; Art Explosion (images).

Local government

records, hard and

electronic property

records, etc.

Buy

er:

Seller:

Property:

Incoming

title order

Title

documents

Pro

blem:

Cleared

Exempt from

coverage

Insured over

x

Commitment

letter

Closing

documents

$

Interested

parties

$

Underwriter

$

Policy

Agents in some states use primarily automated processes, either owning or

purchasing access to a title plant.

13

Because of these plants, the title search

process in these states can be very efficient, which can decrease the

amount of time required to issue a title insurance policy. Some of the most

advanced of these title plants have documents scanned from local

government sources, indexed and cross-referenced by various types of

13

Some state laws, such as those in Iowa and Texas, require title agents or abstractors to

have access to a title plant.

Page 16 GAO-07-401 Title Insurance

identifying information. Four of the title data centers we visited had

electronic records going back 20 years or more. During a tour of one title

plant in Texas, we observed a title examiner obtain nearly all documents

pertinent to the title search and examination in electronic format within

seconds. If the title examiner did not have immediate access to a

necessary document, she would e-mail the owner of that information and

have it sent electronically or through the mail from one of the search

services to which the plant subscribed, usually within 1 day or less. For

this plant, typical turnaround time for a completed title search,

examination, and commitment for a title examiner simultaneously working

on several titles was 2 to 3 days. In another highly automated plant located

in a large urban center, we were told that the typical title search and

examination took about 25 minutes. One of the nation’s largest title

insurers, First American, recently announced that with new software

developments, its agents could produce a fully insured title commitment in

60 seconds for many refinance transactions.

In contrast, in a less-efficient process, agents in some states must

physically search public records, which can add to the time required to

issue a policy. In New York, for example, title plants are rare, and title

agents commonly employ abstractors and independent examiners who

must go to various county offices and courthouses to manually conduct

searches. Including the process of clearing title problems and attorney

review, one underwriter told us that in New York, the typical title

insurance issuance took 90 to120 days for a purchase and 30 to 45 days for

a refinance. Most historical data are proprietary to each underwriter and

are based on previously insured titles. At an underwriter-owned title plant

in an East Coast city, described as typical for the region, we saw that

although the plant held approximately 1.5 million records of previously

insured titles, few records were updated when a new search came in on

that same property. Personnel at the plant said that it was too labor-

intensive to consolidate all of the files, although not updating the files

resulted in a large number of redundancies in records across the plant.

Also, in some states, industry participants told us that delays in recording

and processing at local government offices contributed greatly to

inefficiencies in the issuance process.

Title Agents’

Responsibilities Also

Differ across States

We found that the extent of title agents’ responsibility for claims losses,

involvement in the closing process, and ability to set premiums varied

widely across states. For example, in some states, agents are responsible

for a specific portion of losses on claims. In California and Colorado, the

underwriter-agent agreement stipulates that title agents are responsible for

Page 17 GAO-07-401 Title Insurance

up to the first $5,000 of a title claim.

14

Underwriters said that this

deductible gave agents an incentive to conduct more diligent searches and

examinations. In other states, agents are not responsible for a specific

portion of a claim but may take responsibility for some part or all of it,

especially if the claim is small. According to agents in New York and

Minnesota, it is faster, more efficient, and more customer-friendly for the

agent to handle smaller claims rather than passing them on to the

underwriter. An industry organization said that current, informal agent

claims practices show that agents generally take responsibility for claims

under $2,500. Independent agents told us that the industry is moving

toward more risk borne by the agents. In fact, agent application and

review documents that we obtained from underwriters showed that the

number and amount of claims the agent was responsible for were criteria

insurers used when deciding whether to retain independent agents. One

underwriter told us that although their agents did not have deductibles,

the insurer was able to recover about $10 million in funds from agents on

claims the underwriter had already paid through aggressive follow-up on

and investigation into possible errors on previously paid claims.

Some agents are also involved in more aspects of the closing process. We

found that some agents handled the entire closing process, including the

escrow, while others did not handle the escrow portion. These practices

varied within as well as across states. In California, for example, title

agencies have both underwriter and agent-controlled escrow companies

that handle the full escrow process and actively market those services.

These agencies offer a full package of closing services, from title search,

examination, and clearance to document preparation and disbursement of

funds at the closing. Other title agents were independent from escrow

companies. In some states, such as New York, where it is customary for

the home buyer and seller to have a lawyer present at the closing, title

agents employ closers, whose chief duty is to handle the checks for taxes

and escrow and to record the deed. Similarly, in Illinois, the lawyers

actually serve as attorney-agents and are prohibited by the underwriter

from handling the escrow.

Finally, in some states, title agents determine the amount to charge

consumers for the search and examination portion of the premium, while

in other states, they do not. The states where they do are referred to as

14

California insurance department guidelines say that title agents cannot pay more than

$5,000 of a claim.

Page 18 GAO-07-401 Title Insurance

“risk-rate” states because only the insurance, or risk-based, portion of the

premium is regulated. In these states, state regulators review underwriters’

rates for the risk-based portion of the premium, but the agents set the fees

for search and examination services (generally the larger part of the cost

to consumers) without regulatory review. According to ALTA, 30 states

plus the District of Columbia are considered risk-rate states. The rest of

the states, excluding Iowa, are considered to be all-inclusive because they

incorporate charges for the risk-based portion of title insurance and other

fees, such as those for the search and examination, in the regulated

premium. The premium may or may not include settlement and closing

costs. In these all-inclusive states, agents are not able to determine the

price they will charge for searches and examinations, because they are

required to charge the rates set by the state or the underwriter. Insurers

set their premium rates based on their own expected costs and how much

of the premium they have agreed to split with the agent.

Premiums Are Difficult to

Compare across Markets,

but Appear to Vary

Significantly

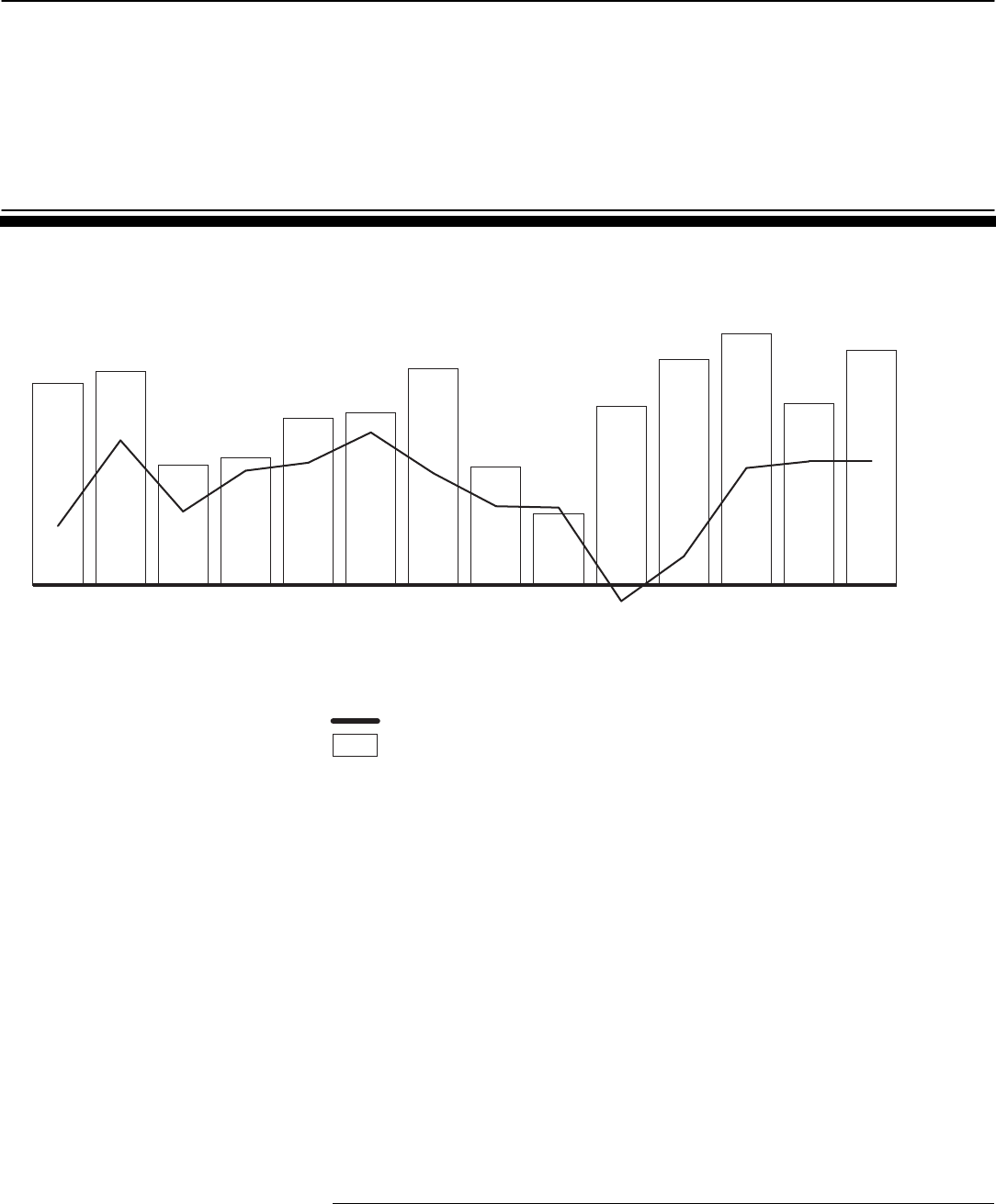

Because title insurance premium rates depend on the amount of the loan

or value of the home being insured, premiums differ widely across states.

Figure 5 shows the premium rates for median-priced homes in major cities

in our sample states.

Figure 5: Title Insurance Premium Rates for a Basic Owner’s Policy on Median-

Priced Homes in Selected Areas, 2005

Des Moines, IA

Dallas, TX

Denver, CO

Chicago, IL

New York, NY

Los Angeles, CA

145,500

147,600

247,100

264,200

445,200

$529,000

700

a

871

1,216

1,025

2,190

$1,587

Median-priced home loan or value Owner’s policy rate

Source: GAO analysis of National Association of Realtors’ and title industry data.

Note: Rates are either from the largest underwriter or are promulgated rates.

a

Lender’s policy rate used in the Iowa data because a rate was not given for the owner’s policy.

Although the premium would be $146, according to Iowa Title Guaranty officials, additional required

services would add approximately another $550, for a total of approximately $700.

Page 19 GAO-07-401 Title Insurance

One reason title insurance premium rate comparisons are difficult is

because, as we previously mentioned, items included in the premium

varied by state. A study from insurance regulators in Florida, where rates

are promulgated and include the risk portion only, noted that what all-

inclusive rates include varies even among the all-inclusive states.

15

According to the study, in Texas and Pennsylvania, the premium includes

the risk portion, search and examination costs, and settlement fees, while

in California, the all-inclusive rate does not include settlement and closing

costs. The Florida study also noted that one state (Utah) includes closing

costs but not searches and examinations, and another state (Illinois)

allows the entire rate to be determined competitively as either risk-based

or all-inclusive.

A national survey conducted by Bankrate.com in 2006 also showed

significant differences in title premiums across states.

16

This survey of the

50 states and the District of Columbia compiled average mortgage closing

costs, including title insurance, search and examination and settlement

costs, and origination fees, using data obtained from as many as 15 of the

largest national lenders’ online quote systems. The survey calculated costs

for a standard $200,000 loan in one Zip Code of the largest urban center in

each state. The data showed costs ranging from a high of $3,887 to a low of

$2,713, with a national average of $3,024. Bankrate.com representatives

attributed most of the difference across states to wide disparities in the

cost of title insurance, which they found varied almost 64 percent, from a

high of $1,164 to a low of $418. The average was $663. However, these data

must be viewed with caution because they do not account for differences

in what could be included in the premium. Moreover, since these data

came from only one Zip Code per state, they may not be representative of

other localities.

Industry officials said that rates vary because of differences in what was

included in the rate and in standard business costs in each area. Nearly all

of the industry participants we spoke with emphasized that title insurance

is a local business, varying both within and across states. They said that

state property, trustee, probate, and estate laws could partially explain the

rate differences. In some states, these requirements make it much more

15

Florida Office of Insurance Regulation, An Analysis of Florida’s Title Insurance Market:

Three Studies That Provide a Comprehensive, Multi-Faceted Review of the Florida Title

Insurance Industry (Tallahassee, FL: July 2006).

16

Closing Costs Survey, http://www.bankrate.com/brm/news/mortgages/ccmain2006a1.asp.

Page 20 GAO-07-401 Title Insurance

expensive to do the search and examination work and clear all of the risks

through the examination process. Experts told us that trying to compare

rates across states would not be meaningful because of the differences in

the components of the premium.

Among the factors raising questions about the existence of price

competition and the resulting prices paid by consumers within the title

insurance industry are the following:

• consumers find it difficult to shop for title insurance, therefore, they put

little pressure on insurers and agents to compete based on price;

• title agents do not market to consumers, who pay for title insurance, but to

those in the position to refer consumers to particular title agents, thus

creating potential conflicts of interest;

• a number of recent investigations by HUD and state regulatory officials

have identified instances of alleged illegal activities within the title

industry that appear to reduce price competition and could indicate

excessive prices;

• as property values or loan amounts increase, prices paid for title insurance

by consumers appear to increase faster than insurers’ and agents’ costs;

and

• in states where agents’ search and examination services are not included

in the premium paid by consumers, it is not clear that additional amounts

paid to title agents are fully supported by underlying costs.

Disagreement exists between title industry officials and regulators over

the actual extent of price competition within title insurance markets, with

industry officials asserting that such competition exists and a number of

regulators stating that a lack of competition ultimately results in excessive

prices paid by consumers.

For several reasons, consumers find it difficult to shop for title insurance

based on price, raising questions about the existence of price competition

in title insurance markets. First, most consumers buy real estate—and

with it, title insurance—infrequently. As a result, they are not familiar with

what title insurance is, what reasonable prices might be, or which title

agents might provide the best service. According to a study commissioned

Multiple Factors

Raise Questions about

the Extent of

Competition and the

Reasonableness of

Prices in the Title

Insurance Industry

Lack of Consumer

Knowledge about Title

Insurance Results in Little

Pressure on Insurers to

Compete on Price

Page 21 GAO-07-401 Title Insurance

by the Fidelity National Title Group, Inc., in response to proposed

regulatory changes in California, it is typically not worth an individual’s

time to become more educated about title insurance, because any

resulting savings would likely be relatively small.

17

That is, the cost to

consumers of becoming sufficiently educated to make an informed

decision is potentially higher than the risk of paying more to a title agent

suggested by a real estate or mortgage professional. However, one

potential consequence of a failure to shop around was noted by several of

the state insurance regulatory officials that we spoke with, who expressed

concern that consumers may not be getting the discounts for which they

are eligible. For instance, insurers may give (1) discounts on mortgage

refinance transactions because the previous search and examination were

fairly recent and (2) discounts to first-time home buyers or senior citizens.

Several title industry officials agreed that consumers might not be aware

of such discounts and may, in some cases, not be receiving discounts to

which they are entitled.

Second, consumers may have difficulty comparing price information from

different title agents because many title agents also charge for services

that are not included in the premium rate, such as fees related to real

estate closing and other administrative fees. In states where title agents

charge separately for search and examination services, such charges can

be as large as the title insurance premium itself. Thus, even if consumers

collected and compared premium rates, which are posted on some states’

Web sites, they might not get an accurate picture of all the title-related

costs they might pay when using a particular agent.

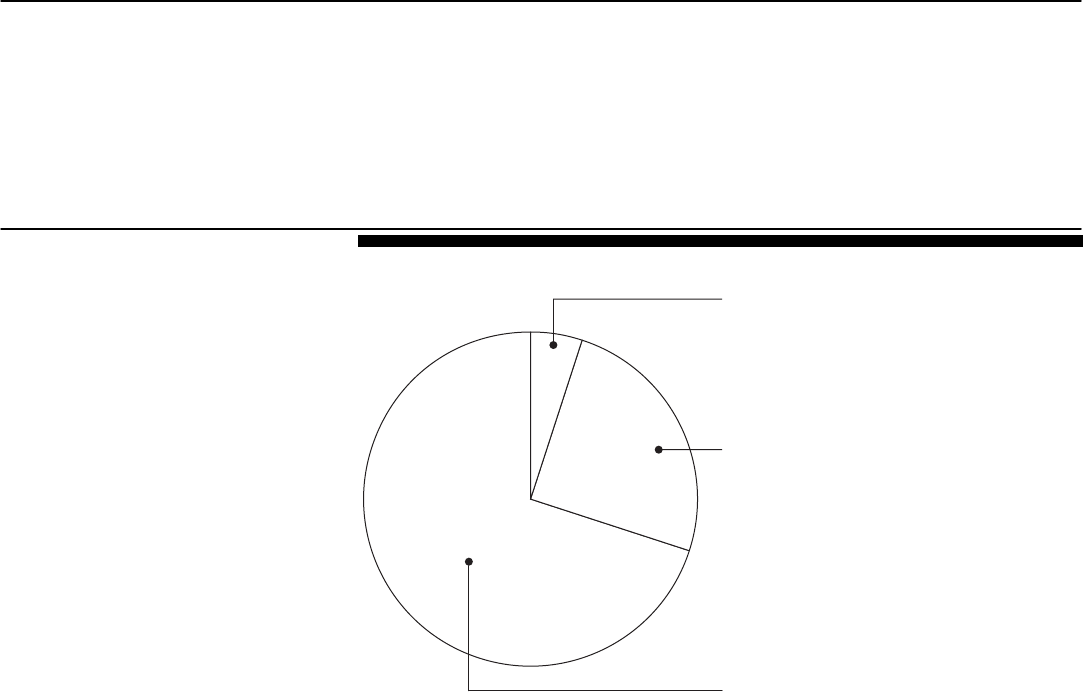

Third, title insurance is a smaller but required part of a larger transaction

that consumers are generally unwilling to disrupt or delay. As we have

seen, lenders generally require home buyers to purchase title insurance as

part of any real estate purchase or mortgage refinancing transaction.

However, purchasing title insurance is a relatively small part of such

transactions. For example, according to an analysis by the Fidelity

National Title Group, Inc., in 2005 in California, on a transaction with a

sales price of $500,000 and a loan amount of $450,000, title insurance

costs, on average, amounted to only 4 percent of total closing costs,

including the real estate agent’s commission (see fig. 6). Even when the

17

Gregory Vistnes, An Economic Analysis of the California Department of Insurance

Proposal to Impose Rate Regulation in the California Title Insurance Industry

(Washington, D.C.: August 2006).

Page 22 GAO-07-401 Title Insurance

seller pays the real estate agent’s commission, title insurance costs are still

small compared with the size of the buyer’s transaction. In addition, it

appears that by the time consumers receive an estimate from the lender of

their title insurance costs as part of the Good Faith Estimate, a title agent

has already been selected, and the title search has already been requested

or completed.

18

To shop around for another title insurer at that point in the

process could also threaten to delay the scheduled closing. According to a

number of title industry officials and state insurance regulators we spoke

with, most consumers place a higher priority on completing their real

estate transaction than on disrupting or delaying that transaction to shop

around for potentially small savings.

18

RESPA requires lenders to provide consumers with an estimate of the costs a consumer

will likely have to pay, called a Good Faith Estimate, prior to the closing of a mortgage

transaction.

Page 23 GAO-07-401 Title Insurance

Figure 6: Average Allocation of Closing Costs in California, 2005

Note: Calculations done using a $500,000 sales price and a $450,000 loan amount. We did not verify

the data supporting this analysis.

HUD publishes an informational booklet designed to help fulfill RESPA’s

goal of helping consumers become better shoppers for mortgage

settlement services, including title insurance. Although this document

provides much useful information, it is generally distributed too late in the

home-buying process to help consumers with respect to title insurance,

and it lacks some potentially useful information. RESPA currently requires

lenders to provide the booklet to consumers within 3 days of the loan

application. HUD officials recognize the need to get this information to

consumers earlier and recommended in a 1998 study that real estate

agents, as well as lenders, provide the information at first contact.

19

4%

4%

P&C insurance

(including home warranty)

12%

13%

64%

2%

Escrow fees

1%

Other costs

Source: Fidelity National Title Group, Inc.

Title insurance

Government taxes/fees

Lender fees

Real estate commission

1,739

975

$331

2,088

5,846

6,150

30,000

Total $47,129

Closing costs

Amount

19

Board of Governors of the Federal Reserve System, Department of Housing and Urban

Development, Joint Report to the Congress Concerning Reform to the Truth in Lending

Act and the Real Estate Settlement Procedures Act (Washington, D.C.: July 1998).

Page 24 GAO-07-401 Title Insurance

Furthermore, RESPA only requires the information to be distributed in a

transaction involving a real estate purchase, and not in other transactions,

such as mortgage refinances, where title insurance is also required by

lenders. The usefulness of the informational booklet is further limited by

the absence of information on the discounts most title insurers provide

and on potentially illegal ABAs.

Because consumers may not have access to potentially useful information

when purchasing title insurance, they may not be able to make well-

informed decisions on the purchase of title insurance. Specifically,

consumers may face difficulty in independently collecting information on

all amounts charged by title agents in order to comparison shop. In

addition, the limitations in the content of HUD’s information booklet and

when consumers receive it can result in consumers’ getting information

too late in the process, thereby hindering their ability to influence the

selection of a title agent or insurer. Moreover, several state insurance

regulators expressed concern that consumers might not be getting all

available discounts because they do not know they are available or that

they are entitled to the discounts. In addition, HUD officials said that the

use and complexity of ABAs in the title industry has increased, and

consumers could benefit from additional information in this area.

Another factor that raises questions about the existence of price

competition is that title agents market to those from whom they get

consumer referrals, and not to consumers themselves, creating potential

conflicts of interest where the referrals could be made in the best interest

of the referrer and not the consumer. Because of the difficulties faced by

consumers in shopping for title insurance, consumers almost always rely

on a referral from a real estate or mortgage professional. In fact, some

insurance regulatory officials we spoke with said they are concerned that

consumers may not even be aware they are able to choose their own title

agent and insurer. According to title industry officials, because of

consumers’ unfamiliarity with and infrequent purchases of title insurance,

it is not cost-effective to market to them. Rather, title agents market to and

compete for referrals from real estate and mortgage professionals.

According to title industry officials, competition among title agents for

consumer referrals is very intense and motivates them to provide excellent

service to real estate and mortgage professionals. This is because if they

do not provide good service, those professionals will send their future

referrals elsewhere. Both title and real estate industry officials told us that

such professionals have a strong interest in customers’ having a good

Title Agents Market Not to

Consumers, but to Those

in a Position to Make

Referrals, Creating

Potential Conflicts of

Interest

Page 25 GAO-07-401 Title Insurance

experience with respect to the portion of a closing conducted by a title

agent, because customers’ experiences there will reflect back on the

professional. As a result, they said, such competition on the basis of

service benefits consumers.

However, this competition among title agents for consumer referrals is

also characterized by potential conflicts of interest, since those making the

referrals may have the motivation to do so based on their own best

interests rather than consumers’ best interests. Real estate and mortgage

professionals interact more regularly with title agents and insurers than do

consumers and, thus, are likely to have better information than consumers

on the prices and quality of work of particular title agents and insurers. To

the extent the interests of those professionals are aligned with those of the

consumers they are referring, the knowledge and expertise of those

professionals can benefit consumers. However, conflicts of interest may

arise when the professional making the referral has a financial interest in

directing the consumer to a particular title agent. Under such

circumstances, the real estate or mortgage professional may be motivated

to make a consumer referral not based on the customer’s best interests but

on the professional’s best interests. For example, a real estate professional

may be a partial or full owner of a title agency, such as through an ABA,

and therefore receive a share of the profits earned by that agency. As such,

the professional may have an incentive to refer customers to that title

agency.

Page 26 GAO-07-401 Title Insurance

In recent years, HUD and state insurance regulators have identified a

number of allegedly illegal activities related to the marketing and sale of

title insurance that appear to be designed to obtain consumer referrals

and, thus, raise questions about competition and, in some cases, the prices

paid by consumers (see sidebar). In addition, several title insurers and

agents told us that they lost market share because they did not provide

some compensation for consumer referrals. The payment or receipt of

compensation for consumer referrals potentially reduces competition

because the selection of title insurer or agent might not be based on the

price or quality of service provided, but on the benefit provided to the one

making the referral. The giving or receiving of anything of value in return

for referral of consumers’ title insurance business is a potential violation

of RESPA and many state laws. For example, it might be illegal for a title

insurer to provide free business services to a realtor in exchange for that

realtor’s referring consumers to the title agent. It might also be illegal for

the realtor to accept those services.

Nonetheless, state and federal regulators have identified a number of

alleged instances of such payments, resulting in those involved paying

over $100 million in fines, penalties, or settlement agreements. Table 1

summarizes these investigations. From 2003 to 2006, insurance regulators

in three of our six sample states had concluded at least 20 investigations

related to the alleged payment of referral fees, involving over 52 entities,